Journey of a Battery

Background

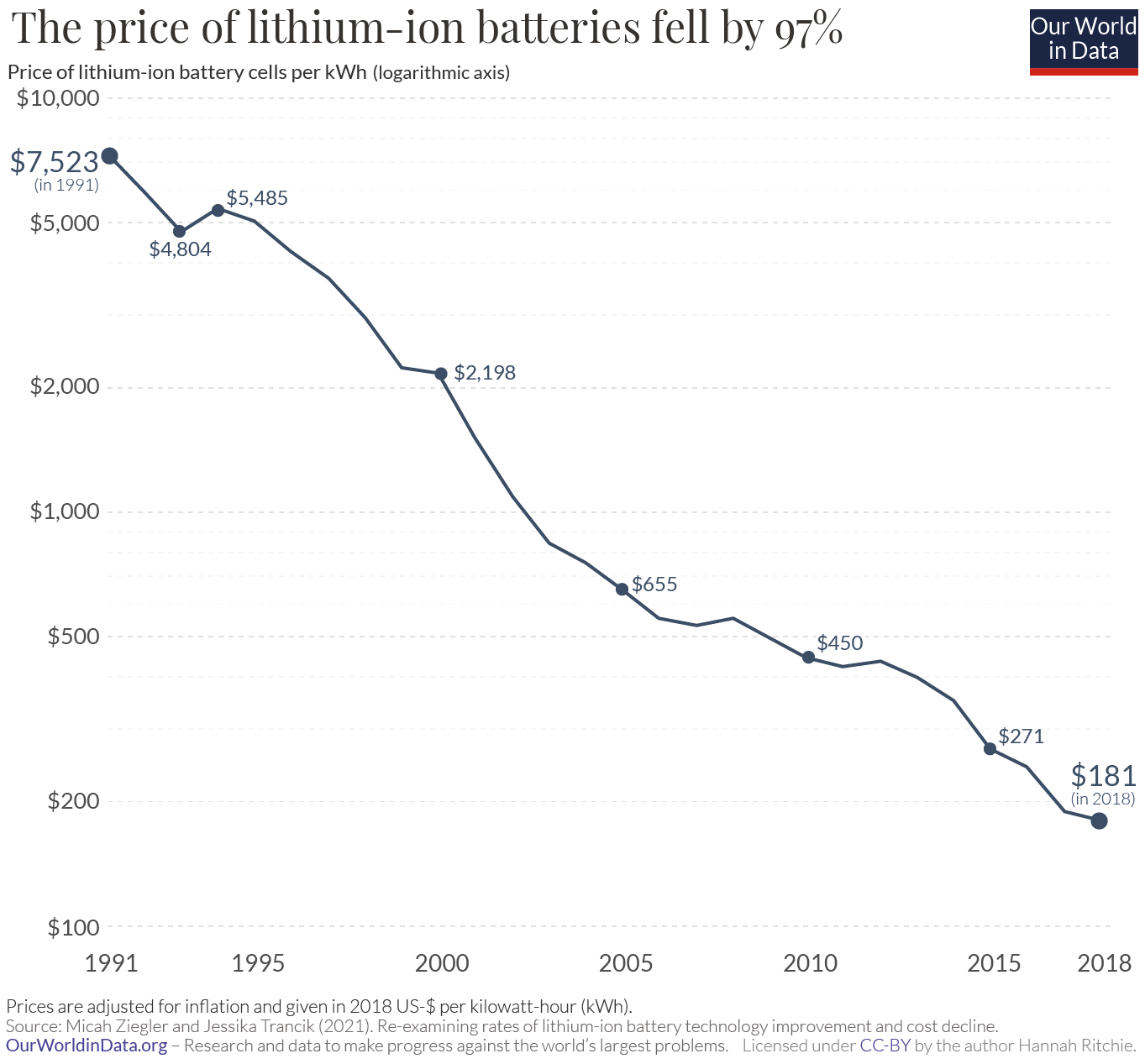

The 2019 Nobel Prize in Chemistry was awarded to the scientists behind the development of Lithium-ion batteries, first introduced to the market in 1991. Since then, within the next 30 years, they’ve only gotten better, with volumetric density increasing threefold and the costs dropping tenfold. So much better that it’s powering the screen you’re reading this on, your car and even your toothbrush.

Source: OurWorldInData

Source: OurWorldInData

This chart is slightly outdated, but gives us something to be proud of — in less than 30 years, the Li-ion battery has found its way to almost every technological equipment we’ve interacted with.

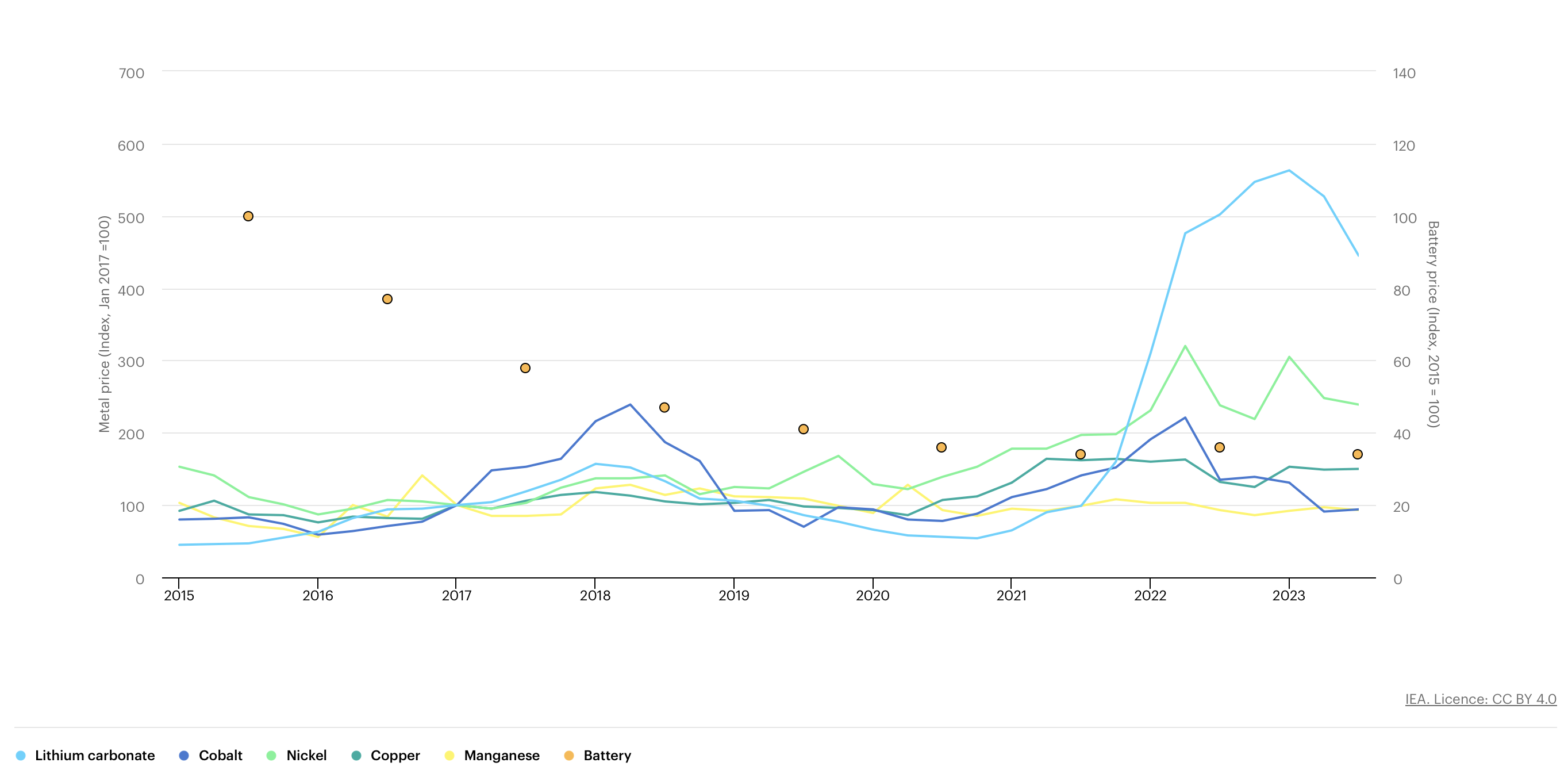

The story for the last couple of years has been a little more muted, primarily due to supply chain shocks resulting from the pandemic, rising demand as the global economy started to recover and the Russia-Ukraine war (tough to keep your supply chain buzzing when there’s a war raging the background) among other factors.

Source: IEA

Source: IEA

The chart above suggests that battery prices have plateaued. But there are telling signs that could make us expect further drops in prices, with average battery pack prices falling to $139/kWh as of November 2023, a 14% drop from $161/kWh in 2022. From IEA,

The combination of an expected 40% increase in supply and slower growth in demand, especially for EVs in China, has contributed to this trend. This drop – if sustained – could translate into lower battery prices.

For a long time, the accepted standard to reach total cost of ownership parity with ICE vehicles was battery pack prices of USD 100/kWh, which corresponds to battery cell prices of USD 80/kWh. Picture this as the financial ‘sound barrier’ we’ve been racing to break. We just hit a record low of USD 139/kWh a couple of months ago, so presumably, we’re well positioned to hit our targets pretty soon.

But there’s more. Companies like Renault and Ford have publicly announced targets of $80/kWh by 20306. Meanwhile, the US Department of Energy is moving the goalposts even further, setting their sights on a groundbreaking $60/kWh. Quoting David Howell, the Principal Deputy Director at DoE6:

By getting to $60/kWh, an EV’s total cost of ownership will be 26 cents a mile. Combustion is 27 cents.

So with all this mind, can we get there reasonably soon?

What goes into a Li-ion battery?

Costs incurred

Source: Benchmark Mineral Intelligence

Source: Benchmark Mineral Intelligence

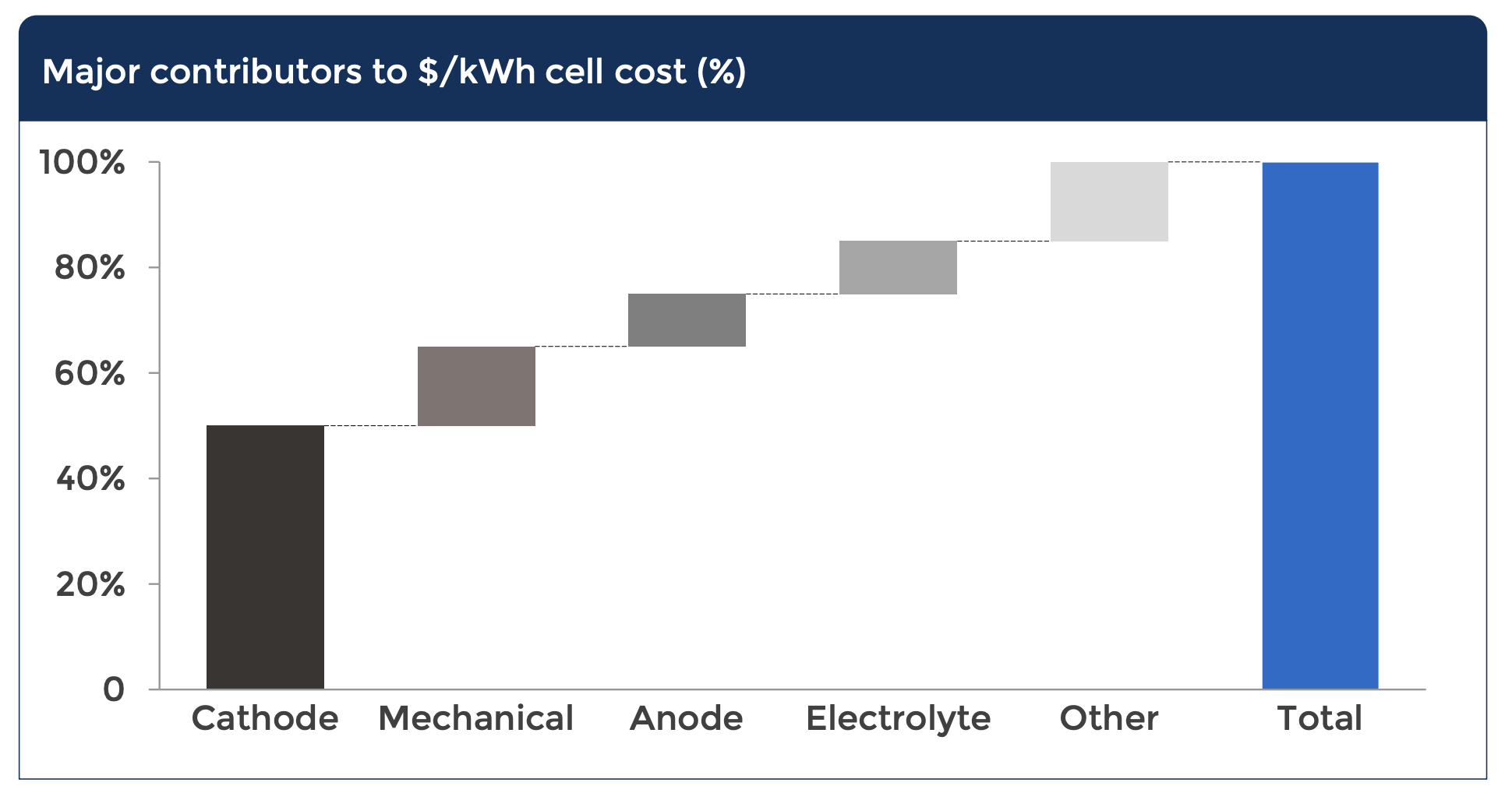

Reducing costs at the cell level is akin to fine-tuning an intricate machine. The focus? Managing supply chain expenses for key materials and enhancing manufacturing efficiency – think less waste, more power.

Interestingly, investments in R&D on materials and chemistry were key to the price decline, while economies of scale contributed somewhat less.

Source: RSC

Source: RSC

A deep dive into the data reveals a striking insight: an R² value of 0.96 illustrates a strong correlation between price decline and the number of patents filed. In simpler terms, more innovation equals lower costs. This contrasts with an R² of 0.88 for price against market size, suggesting that while growing demand helps, cutting-edge research is the real game-changer.

When it comes to cost contribution, the cathode takes center stage. It’s not just another component; it’s the epicenter of both innovation and expense, accounting for more than half of the total production cost of battery cells. So let’s dive a little deeper into that, and see where we’re going.

Cathode

The cathode represents over 50% of the total cost in producing battery cells, with key components like Lithium, Nickel, and Cobalt accounting for approximately 50-65% of the cost, fluctuating with raw material prices. These metals are not only expensive but also come with several other challenges. For instance, consider Cobalt. Battery manufacturers are actively seeking alternatives to cobalt due to several reasons:

-

Cost: Cobalt is the second most expensive mineral used in batteries. While Lithium carbonate currently holds the top spot, its price is expected to decrease as supply begins to meet the demand deficit.

-

Supply and Geopolitical Risk: More than 60% of the world’s cobalt supply originates from the Democratic Republic of Congo (DRC), a region plagued by political instability and ethical concerns in mining practices2.

-

Scarcity: Forecasts indicate significant regional disparities in cobalt demand and supply, as well as supply security levels. This imbalance is expected to lead to a shortage between 2028 and 20333.

So, generally, we want to move towards Cobalt-free batteries, but it’s tough and will take more than a village to do so4. One strategy to solving for short term availability of Cobalt while mitigating risks is pushing for a circular economy (more on that later). Some of the problems mentioned above are not unique to Cobalt.

Why can we get there?

- More R&D efforts - government grants, startup funding

Globally, governments are ramping up their commitment to incentivize research and development for the sector. In the US, the DoE’s recent injection of $131mn exemplifies this trend, focusing on enhancing electric vehicle (EV) batteries and charging systems5. Across the Atlantic, the UK government’s pledge of over $2.5bn between 2025 and 2030 for zero-emission vehicle technologies underscores the international urgency in this field[6].

However, this wave of enthusiasm isn’t without its challenges. Germany’s R&D alliance, representing its battery industry, has voiced concerns over potential cuts in government funding, highlighting the delicate balance between fiscal policy and technological advancement7. Similarly, in India, the Confederation of Indian Industry’s recent report emphasizes the critical need for incentivizing R&D in battery technology to stay competitive in the global market8.

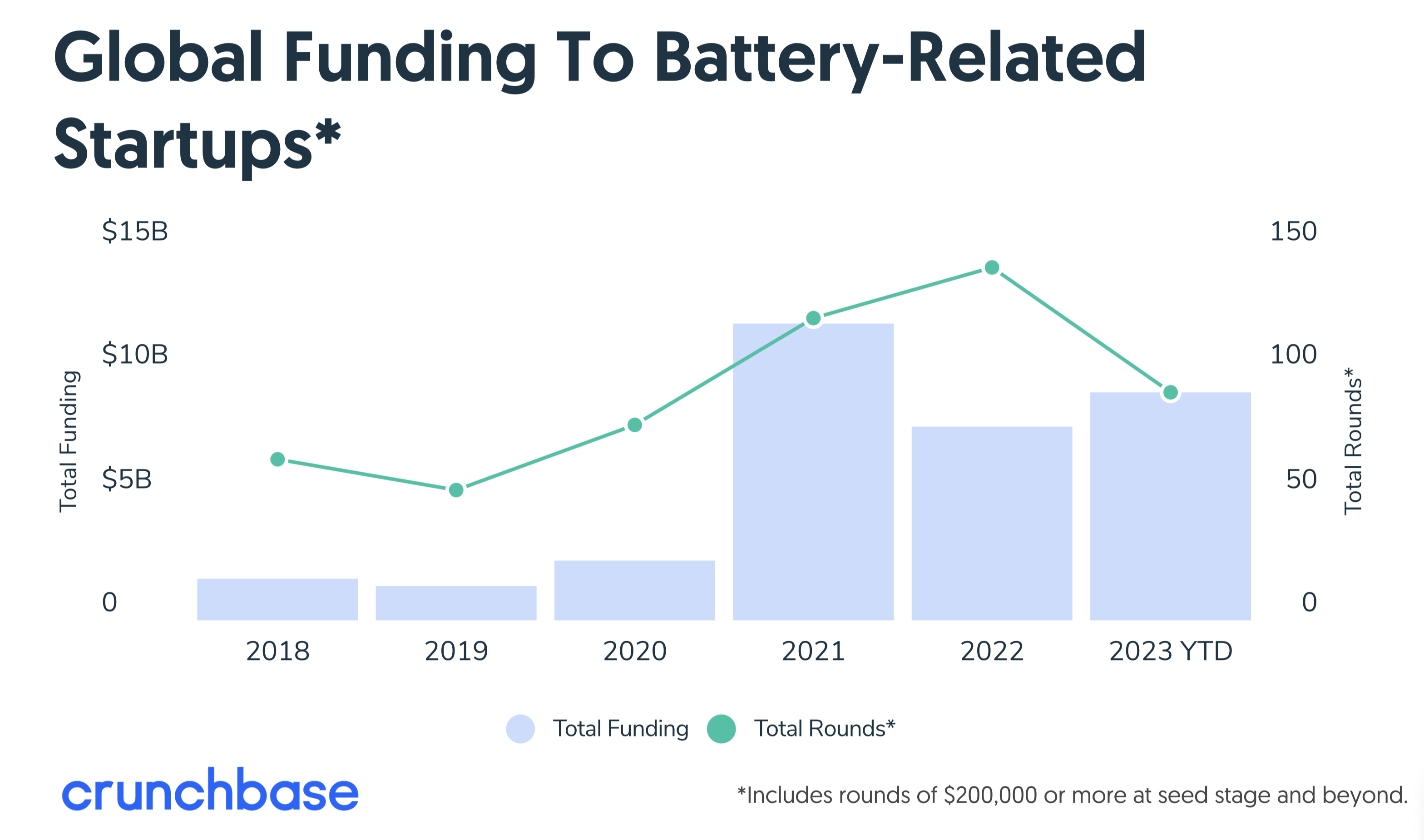

Coming to private funding, battery tech startups fared better than the average startup. While the total number of funding rounds for battery-related startups decreased in 2023, the actual funding amount saw an increase.

Source: Crunchbase

Source: Crunchbase

Source: Crunchbase

Source: Crunchbase

This suggests that despite a reduction in the frequency of investments, the average deal size was larger, signaling strong investor confidence in the sector. This trend may well continue, owing to certain pecularities of the sector. Form the inimitable Noah Smith9:

[The] big challenge is that many forms of deep tech — biopharma and other research-intensive industries — is that the long lead time and high up-front cost presents big challenges for the traditional low-cost, fast-scaling VC financing model. Battery-driven tech, however, may prove an exception. The fact that the basic research is being done in universities frees up VCs to fund applications instead of labs. And the fact that energy portability allows gadgets to adapt themselves to existing infrastructure means that investors won’t have to tussle so much with regulators or fund expensive modifications to the built environment.

- Tools for managing price volatility

Only recently did market participants gain access to lithium carbonate futures7. With a new tool for managing price risk, we should expect a more stable and predictable market environment for lithium carbonate. This development could lead to better financial planning for companies involved in lithium production and usage. Additionally, it may attract further investment into the lithium market, as the ability to hedge can make it a more appealing option for portfolio diversification. Over time, this could also provide a clearer picture of supply and demand dynamics as reflected in the futures pricing, potentially driving more informed decision-making across the industry. For investors, what can be seen in a Bloomberg terminal gives a good night’s sleep (if that’s possible).

- Developing a circular economy

While Lithium and other metals can be used as part of a sustainable energy plan, they shouldn’t be the ultimate solution for all our energy woes - they’re depletable after all. Scarcity concerns coupled with unsafe disposal practices have prompted companies to invest in recycling solutions, a nascent industry so far. Apart from safety benefits, recycling offers companies an opportunity to derisk their supply chains by reusing the same materials in the future. Regional approaches to these challenges vary significantly, as seen in India’s battery ecosystem development. Recyclability is an absolute game-changer.

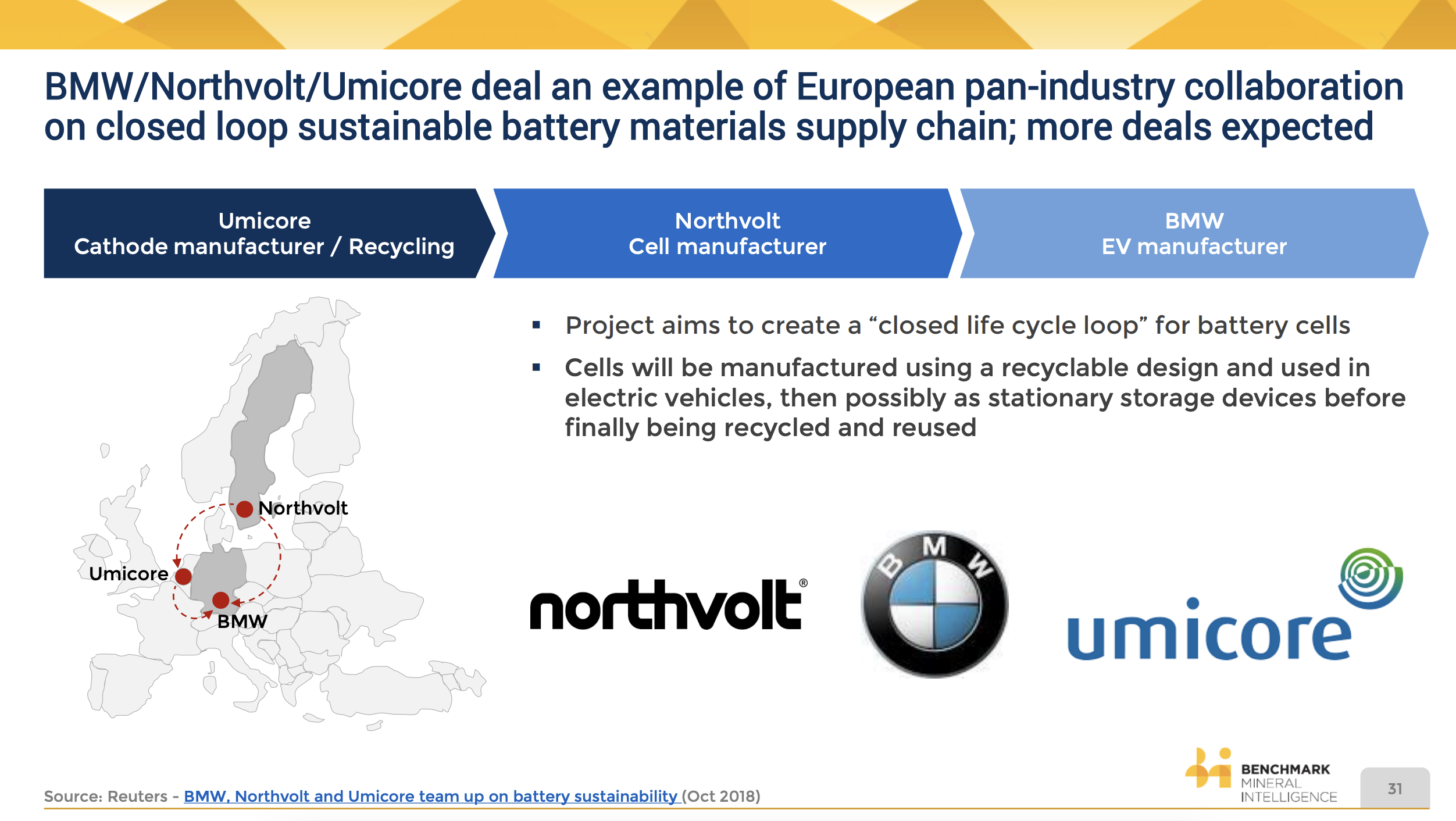

Regulatory push from countries is providing a fillip to setting up feasible recycling plants. Europe has initiated stringent battery recycling mandates, mandating producers to not only reclaim Li-ion batteries but also incorporate a minimum of 5% recycled cobalt and lithium starting from this year, a proportion set to escalate to 70% by 2030. In parallel, the United States introduced the Inflation Reduction Act, allocating significant subsidies to localize the EV supply chain and reduce reliance on critical metals sourced from abroad. This includes substantial financial support for recycling initiatives, exemplified by the recent allocation of $2bn as federal loans to firms like Redwood Materials for enhancing recycling processes. With lucrative incentives, industry players are beginning to plow more money into localizing supply chains. An example is the BMW, Northvolt and Umicore deal11, announced way back in 2018 (!), where the collaboration aims to create a closed battery lifecycle loop.

Source: Benchmark Mineral Intelligence

Source: Benchmark Mineral Intelligence

Transitioning towards any new technology comes with it’s set of challenges. Especially when transitioning something as ubiquitous and essential as energy. And although we’re getting there, we need to do more. More investments, more regulations and more innovation will go a long way in ensuring we keep our Earth inhabitable for the next generation.